What is Digital Onboarding and How Does It Work?

Opening a bank account used to mean booking an appointment, printing out documents, and sitting across a desk from someone who took your passport and made a photocopy of it. Today, that same process can be done from your sofa in under ten minutes.

But what’s actually happening behind the scenes when you sign up for a new service online? This article breaks down exactly what digital onboarding is, how it works step by step, and why getting it right matters more than ever.

What Is Digital Onboarding?

Digital onboarding is the process of bringing a new customer (or user) into a business relationship entirely online without ever needing to manually process paperwork and in-person interaction.

Practically speaking, before granting access to a product or service, a business verifies a new customer’s identity and collects the information it needs – all through digital channels. By replacing the slow, paper-based experience of the past, digital onboarding offers a secure, automated digital flow that can be completed from anywhere.

Digital onboarding is most commonly used in banking, insurance, telecommunications, e-commerce, mobile services, and more. But it’s especially critical in regulated sectors like financial services, where businesses are legally required to know who their customers are before opening an account or providing access to funds.

Often a critical part of Know Your Customer (KYC) protocols, the customer onboarding process typically involves submitting identity documents, providing biometric data (such as a selfie or fingerprint), and undergoing background or sanctions-list checks. While the specific steps may vary by organization or sector, the goal is always the same: to verify a user’s identity securely, efficiently, and in compliance with regulations.

In a world where expectations for speed and convenience are higher than ever, the onboarding experience can make or break a customer relationship before it even starts. Source

Finally, in today’s world customer expectations are higher than ever. So, the onboarding experience can make or break a customer relationship before it even starts.

How Does Digital Onboarding Work?

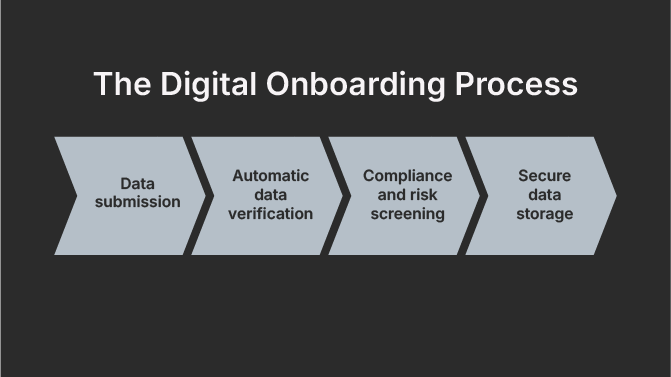

Most digital onboarding processes follow a series of steps that gradually establish trust, capture data, verify users, and satisfy regulatory requirements.

STEP 1. Data Submission

In a digital onboarding flow, a potential customer or user will typically be asked to provide basic personal information: name, date of birth, address, and contact details, along with one or more identity documents, such as a passport, national ID card, or driver’s license.

This is where digital document upload and remote identity verification come in. Rather than handing over a physical document, a user can photograph it with their phone or upload a scan. Many systems then ask the user to perform a liveness check, which involves taking a live selfie, sometimes with a specific head movement or blink. Then, the system confirms that a real person is submitting the documents in real time, not just a photo of a photo.

STEP 2. Automatic Data Verification

Once the user’s documents are submitted, automated validation kicks in. This is the step where the system does what a bank clerk would previously have done manually, but in seconds rather than days, and usually with the help of AI.

Optical Character Recognition (OCR) technology reads the text on your document and extracts key data: your name, date of birth, document number, and expiry date. The system then cross-references this against the data you typed in to check for inconsistencies. Biometric comparison tools match the user’s selfie to the photo on their ID. And advanced algorithms check whether the document itself appears genuine, by looking at fonts, security features, holograms, and other markers that are difficult to forge.

STEP 3. Compliance and Risk Screening

This step is about compliance. After the customer passes biometric verification, the system then checks for any further regulations and performs validity checks, such as Know Your Customer (KYC) and Anti-Money Laundering (AML) screenings, scanning against watchlists, sanctions, and Politically Exposed Persons (PEP) databases.

All of these actions are automated. Globally, these checks are mandatory and are governed by frameworks set by bodies such as the Financial Action Task Force (FATF), the EU’s Anti-Money Laundering Directives (AMLD), the US Bank Secrecy Act (BSA), and the UK’s Money Laundering Regulations.

For example, the system checks the document against sanctions or PEP lists to examine the customer’s risk level or lost and stolen registries to ensure the document is currently in the possession of the rightful owner.

STEP 4. Secure Data Storage

Once verification and compliance checks are complete, all the information gathered is stored securely in the business’s systems, which is a legal obligation in most regulated industries. Under regulations like the EU’s General Data Protection Regulation (GDPR), the responsibility for storing customers’ data lies with businesses. Thus, customer data must be securely encrypted, access-controlled, and retained only for as long as legally required. Customers also have rights over their data, including the right to access it or request its deletion in certain circumstances.

Types of Digital Onboarding

Depending on the industry, the risk level, and the technology available, businesses implement onboarding in different ways. Here are the main types of onboarding methods companies can adopt for a frictionless onboarding experience:

Automated Digital Onboarding Process

A fully hands-off method, it uses AI and APIs to handle everything from upload to approval in minutes. From data submission to compliance checks to account activation, the entire customer journey is handled by automated systems with no human involvement.

Ideal for low-to-medium risk users, this approach reduces manual work, eliminates human error, and provides an onboarding flow that is fast and feels seamless – the key criteria of a great customer experience.

Best for: Digital banking apps and financial institutions looking to onboard large volumes of new account holders without compromising on security or speed.

Assisted Digital Onboarding Process

In this model, automation handles most of the process, but a human agent is available when needed. This might happen when a document is unclear, when the risk assessment flags an unusual profile, or when a customer is struggling with the process.

Through a secure, remote video call, KYC agents guide new customers through the customer onboarding process in real time. Users simply show their ID to the camera while the agent assesses its validity and performs liveness checks.

Best for: Financial institutions that offer more complex products like mortgages, business accounts, or investment platforms, and onboard higher-risk clients or need to meet regional regulations requiring human oversight. It’s a perfect solution when you want the convenience of digital verification, but still need the assurance of human judgment.

NFC-Based Digital Onboarding Process

One of the most secure forms of digital customer onboarding, the Near Field Communication (NFC) technology allows a smartphone to read the chip embedded in modern biometric passports and national ID cards. Rather than photographing a document and relying on OCR, the system reads the data directly from the chip, which is harder to tamper with and produces more accurate results.

Best for: Regulated industries and engagement platforms where user trust and data security are paramount. It’s a faster and more secure way to verify identity, particularly for high-value financial services.

Manual Digital Onboarding Process

At the other end of the spectrum, some businesses still rely on manual review of digitally submitted documents. A customer uploads their information online, but a human agent then checks everything before the account is approved. This approach is slower and more resource-intensive than automation, as well as prone to greater risk of human error and inconsistency.

Best for: Smaller businesses that haven’t yet invested in automated verification tools, or those in highly regulated niches with more complex customer onboarding scenarios, where additional Customer Due Diligence (CDD) is required.

Benefits of Automating Digital Onboarding

The size of the digital onboarding market is growing from $10.1 billion in 2023 to a predicted $31.2 billion by 2033, which stands at a 12.1% CAGR. The popularity of moving from paper-based or manual processes to automated digital onboarding is due to the positive effects it creates for both businesses and customers, such as operational efficiency, better compliance, and increased customer satisfaction.

Fewer Errors, Greater Accuracy

It’s no surprise that when humans review documents manually, mistakes happen. Typos go unchecked, documents are misread, and inconsistencies are sometimes missed. It’s not the case for the automated digital customer onboarding that applies the same rules every time, without fatigue.

AI-powered validation tools, biometric checks, and OCR tools extract data from documents with high precision, while algorithmic checks catch discrepancies that a tired KYC reviewer might miss at the end of a long shift.

Human errors are a significant problem in compliance, especially in industries like digital banking and fintech, because even a single missed sanction or an improperly verified identity document can lead to serious regulatory penalties.

Cost and Time Savings

Manual onboarding is expensive because every application that requires human review takes time, and time, as we all know, costs money. Automation dramatically reduces the cost per application and allows businesses to scale without needing to hire a proportionally larger compliance team.

It was estimated that almost 330 million new bank accounts were to be opened via digital onboarding in 2025, up from 184 million in 2020. Now, that’s a scale that would be impossible to manage without automating identity verification. What might take a human specialist several hours or even days can now be completed in mere minutes.

Automated digital identity verification reduces onboarding time up to 50-68%, freeing staff and trimming costs, which is extremely vital when 90% of firms see drop-offs otherwise.

The potential cost reduction in onboarding costs by using digital ID-enabled processes is 90%. Source

Better Customer Experience

It’s a fact: customers prefer simplicity and speed. And vice versa – a lengthy or confusing customer onboarding experience can drive users away before they even start. Research shows that 7 in 10 customers will switch to a competitor if they feel the onboarding process is too complicated.

A smooth, well-designed digital onboarding flow removes friction, sets a positive first impression, and signals to the customer that the business values their time. 86% of customers say they will remain loyal to a company if onboarding and continuous education are provided.

Especially for digital-first brands and engagement platforms, smooth digital onboarding is key to maintaining momentum and keeping users invested from the very first interaction. So, getting the first experience right is very important because it leads to better customer retention and higher satisfaction throughout the user journey.

Secure and Organized Data Management

Digital systems store data consistently and in searchable, structured formats. This makes it far easier to retrieve records when needed – whether for a compliance audit, a regulatory inquiry, or a customer service request.

And when combined with robust encryption and access controls, automated data management greatly reduces the risk of data breaches and ensures that businesses can demonstrate compliance with data protection obligations.

For digital banking providers and regulated industries, this means enhanced data protection, better auditability, and compliance. Digital records are easier to search, organize, and share internally, ensuring your teams have the right information at the right time.

Evaluating New Users Efficiently

Digital onboarding systems go beyond simple identity verification by instantly assessing the risk a new user poses to a business. A smart digital onboarding process links ID proof to AML scans seamlessly, spotting fraud without slowing everyone down.

By analyzing factors like location, profession, and fraud patterns, these systems provide immediate approval for most applicants while flagging high-risk profiles for manual review.

This risk-based approach is specifically recommended by FATF and other regulatory bodies as the most proportionate way to apply compliance resources. Not every customer poses the same risk, so it doesn’t make sense to subject everyone to the same intensive scrutiny.

The global cost of identity fraud was projected to exceed $50 billion in 2025. Source

Keeping Data Safe and Compliant

Collecting and storing personal data comes with serious obligations. That’s why digital onboarding processes must be designed with compliance at their core, not just to meet regulatory requirements, but because customers trust businesses with sensitive personal information, and that trust needs to be earned and maintained.

In practice, this means that:

- Data must be stored with appropriate encryption

- Access to customer records must be restricted to those who genuinely need it

- Data retention policies must comply with local laws, like GDPR in the EU

For financial services, AML regulations often require that customer due diligence records be kept for a minimum of five years after the end of a business relationship.

Digital onboarding systems that are built with compliance in mind create detailed audit trails: records of when data was collected, who accessed it, what checks were run, and what decisions were made. This audit trail is invaluable when regulators come knocking.

When to Bring in the Experts

Digital onboarding touches multiple disciplines at once: technology, legal compliance, user experience design, data security, and fraud prevention. For most organizations, especially those in regulated industries, getting it right requires specialist input.

While automation handles the bulk of the onboarding process, some scenarios still benefit from a human touch:

- High-risk cases flagged during screening

- Regulatory exceptions requiring manual checks

- Edge cases involving document anomalies or unusual user behavior

Hybrid models that combine automation with expert review provide both speed where it counts and precision when it matters.

Pro tip: If your organization is expanding into new markets, the complexity multiplies. Compliance requirements differ significantly between the EU, the US, the UK, and other jurisdictions. What works in one market may not satisfy regulators in another. So, getting expert guidance before you build or expand, rather than retrofitting compliance after the fact, is almost always the more cost-effective approach.

The Future of Digital Onboarding

Digital onboarding is a dynamic process, as it evolves alongside new technologies such as advanced biometrics, AI-powered identity verification, and adaptive risk-based verification. These trends are making onboarding both faster and more secure, setting new expectations for how quickly and confidently businesses can welcome new users.

From reducing friction for customers to enhancing compliance and cutting costs for organizations, it’s safe to say that digital onboarding is the preferred digital experience everywhere. So, what’s left is to choose the most appropriate digital onboarding solution for your business.

FAQ